Are You Taking Full Advantage of Everything We Offer?

One of the greatest compliments we receive is when clients tell us they sleep better knowing they have a trusted financial team looking out for them. That peace of mind is exactly what we strive to provide.

Movement: One of the Most Powerful Investments in Your Health

In the world of health and wellness, there is never a shortage of new trends. One year it is a specific diet. The next year it is supplements, fasting strategies, cold plunges, or the latest “miracle” fitness program. While some of these ideas may offer benefits, one principle has remained remarkably consistent through decades of medical research.

Does the Economy Drive the Markets—or Do the Markets Drive the Economy?

It’s a question that comes up frequently, especially during periods of volatility: are financial markets simply a reflection of the underlying economy, or do they play a more active role in shaping it? The answer, perhaps unsurprisingly, is not either/or—but both. Understanding this relationship can help investors better interpret headlines, manage expectations, and make more thoughtful long-term decisions.

How Social Security Adjusts for Inflation And Why It May Still Fall Short

There has already been much chatter looking ahead to 2027, Social Security recipients will once again receive a cost-of-living adjustment (COLA) designed to help offset inflation. While the official figure will not be announced until October 2026 by the Social Security Administration, early projections suggest a more moderate increase compared to the elevated adjustments seen in recent years.

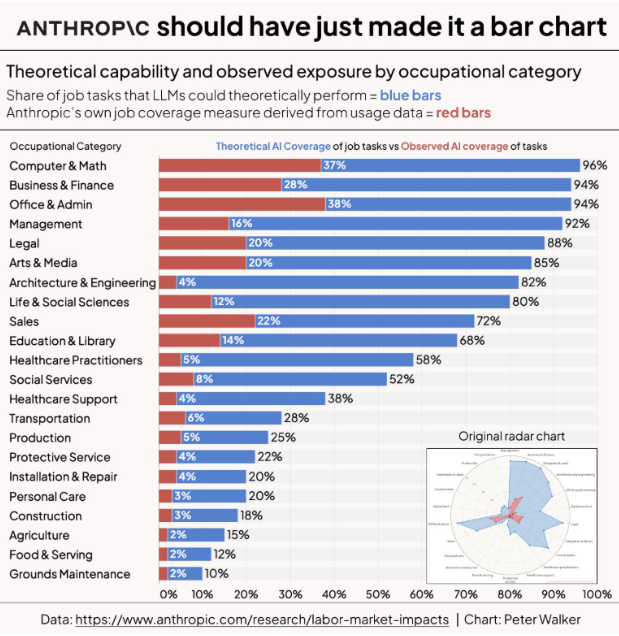

The 100-Year Fiscal Problem: Who Pays for Government in an Age of Ai/Robotics?

For most of modern history, government finances have relied heavily on taxes from human labor. Individuals work, earn wages, and pay income and payroll taxes. Those taxes fund infrastructure, national defense, education, and social programs like Social Security and Medicare. The structure of government finance has therefore been closely tied to the structure of the labor market. When more people work and earn wages, tax revenues increase. When employment declines, tax revenues fall.

Are Pensions a Pyramid?

For generations, many workers have viewed pensions as one of the most secure forms of retirement income—an employer-backed promise of monthly payments for life. But when pension plans become underfunded, the rules surrounding those benefits can change—sometimes dramatically. While pensions are not pyramid schemes, severely underfunded plans can begin to exhibit some uncomfortable similarities that raise important questions about how these systems function.

Prediction Markets: Forecasting the Future—Or Just Another Form of Speculation?

In recent years, a new type of marketplace has been gaining attention in financial and technology circles: prediction markets. While they may sound futuristic, the concept is straightforward. Prediction markets allow people to place small wagers on the outcome of future events—from elections and economic data releases to movie box office results and even the weather.

Optimizing Your Roth IRA: Smart Strategies for Tax-Free Retirement Growth

For many investors, the Roth IRA represents one of the most powerful tools available in retirement planning. Unlike traditional retirement accounts, such as IRAs and 401(k)s, qualified withdrawals from a Roth IRA are completely tax-free, and the account is not subject to required minimum distributions (RMDs) during the owner’s lifetime. Just as important, the assets within a Roth IRA can continue compounding and growing tax-free for the rest of the owner’s life, allowing the full value of the account to work uninterrupted by annual taxation or forced withdrawals. These features make Roth assets uniquely valuable—especially for individuals who expect higher tax rates in the future or who want to maximize and preserve long-term, tax-efficient wealth for themselves and ultimately for their heirs.

A Framework for Evaluating Permanent Policies

Many people in their 30s-40s have been sold a concept of life insurance as an investment vehicle. Especially in periods of market volatility or rising tax rates, permanent life insurance often resurfaces in financial conversations as an “alternative asset class.” It is presented as tax-advantaged, conservative, and contractually backed by guarantees. In certain circumstances, it can absolutely play a valuable role in a comprehensive plan. However, the most important starting point is this: life insurance is first and foremost a risk management tool(insurance). Only in specific situations does it make sense to evaluate it primarily as an accumulation vehicle. We’ll cover the key points to consider, and if you need help deciding, we’re always here to help you evaluate your options.

The First 5 Years of Retirement Matter More Than You Think

For many people, retirement is imagined as a long, steady phase of life—one where the big decisions are made up front and everything else simply unfolds. In reality, retirement is anything but static. And while every year matters, the first five years often matter more than the rest.

5 Investment Market Truths

The economy does not operate in a constant, stable environment. Instead, it moves through distinct regimes such as reflation, inflation, stagnation, and deflation. Each regime rewards different types of assets.

The Power of Coordination: Why Investments, Taxes, and Planning Should Work Together

When it comes to managing money, most people don’t make bad decisions, they make isolated ones.

An investment decision made without considering taxes.

A tax decision made without regard to long-term goals.

A retirement plan based on assumptions that quietly drift out of date.

Each decision may be reasonable on its own. But when financial choices are made in silos, inefficiencies tend to build over time, often without anyone realizing it.

True financial confidence isn’t created by a single strategy or product. It comes from coordination: ensuring that investments, taxes, and planning are aligned and working together toward the same objectives.

The Retirement Paycheck: How Income Really Works After Work

One of the biggest mental shifts retirees face isn’t stopping work—it’s changing how income shows up in their lives.

During your working years, income is simple. You earn a paycheck, taxes are withheld, and what lands in your bank account is what you spend. Retirement works differently. There’s no employer, no automatic paycheck, and no one-size-fits-all formula. Instead, income must be designed, coordinated, and managed intentionally.

That’s why we often refer to retirement income as a retirement paycheck—because it should be predictable, sustainable, and aligned with your lifestyle, even though it doesn’t come from a single source.