Are You Taking Full Advantage of Everything We Offer?

One of the greatest compliments we receive is when clients tell us they sleep better knowing they have a trusted financial team looking out for them. That peace of mind is exactly what we strive to provide.

How Social Security Adjusts for Inflation And Why It May Still Fall Short

There has already been much chatter looking ahead to 2027, Social Security recipients will once again receive a cost-of-living adjustment (COLA) designed to help offset inflation. While the official figure will not be announced until October 2026 by the Social Security Administration, early projections suggest a more moderate increase compared to the elevated adjustments seen in recent years.

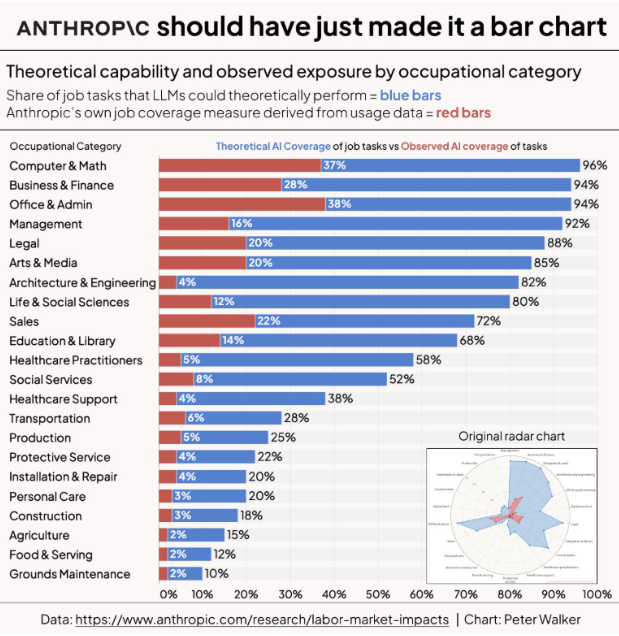

The 100-Year Fiscal Problem: Who Pays for Government in an Age of Ai/Robotics?

For most of modern history, government finances have relied heavily on taxes from human labor. Individuals work, earn wages, and pay income and payroll taxes. Those taxes fund infrastructure, national defense, education, and social programs like Social Security and Medicare. The structure of government finance has therefore been closely tied to the structure of the labor market. When more people work and earn wages, tax revenues increase. When employment declines, tax revenues fall.

Are Pensions a Pyramid?

For generations, many workers have viewed pensions as one of the most secure forms of retirement income—an employer-backed promise of monthly payments for life. But when pension plans become underfunded, the rules surrounding those benefits can change—sometimes dramatically. While pensions are not pyramid schemes, severely underfunded plans can begin to exhibit some uncomfortable similarities that raise important questions about how these systems function.

Prediction Markets: Forecasting the Future—Or Just Another Form of Speculation?

In recent years, a new type of marketplace has been gaining attention in financial and technology circles: prediction markets. While they may sound futuristic, the concept is straightforward. Prediction markets allow people to place small wagers on the outcome of future events—from elections and economic data releases to movie box office results and even the weather.

Optimizing Your Roth IRA: Smart Strategies for Tax-Free Retirement Growth

For many investors, the Roth IRA represents one of the most powerful tools available in retirement planning. Unlike traditional retirement accounts, such as IRAs and 401(k)s, qualified withdrawals from a Roth IRA are completely tax-free, and the account is not subject to required minimum distributions (RMDs) during the owner’s lifetime. Just as important, the assets within a Roth IRA can continue compounding and growing tax-free for the rest of the owner’s life, allowing the full value of the account to work uninterrupted by annual taxation or forced withdrawals. These features make Roth assets uniquely valuable—especially for individuals who expect higher tax rates in the future or who want to maximize and preserve long-term, tax-efficient wealth for themselves and ultimately for their heirs.

A Framework for Evaluating Permanent Policies

Many people in their 30s-40s have been sold a concept of life insurance as an investment vehicle. Especially in periods of market volatility or rising tax rates, permanent life insurance often resurfaces in financial conversations as an “alternative asset class.” It is presented as tax-advantaged, conservative, and contractually backed by guarantees. In certain circumstances, it can absolutely play a valuable role in a comprehensive plan. However, the most important starting point is this: life insurance is first and foremost a risk management tool(insurance). Only in specific situations does it make sense to evaluate it primarily as an accumulation vehicle. We’ll cover the key points to consider, and if you need help deciding, we’re always here to help you evaluate your options.

The Power of Coordination: Why Investments, Taxes, and Planning Should Work Together

When it comes to managing money, most people don’t make bad decisions, they make isolated ones.

An investment decision made without considering taxes.

A tax decision made without regard to long-term goals.

A retirement plan based on assumptions that quietly drift out of date.

Each decision may be reasonable on its own. But when financial choices are made in silos, inefficiencies tend to build over time, often without anyone realizing it.

True financial confidence isn’t created by a single strategy or product. It comes from coordination: ensuring that investments, taxes, and planning are aligned and working together toward the same objectives.

Is Now the Time to Work With a Financial Planner?

If you’ve been asking yourself whether to hire a financial planner, the short answer is: probably. The long answer is worth a few minutes of reading, because research shows professional advice delivers measurable benefits beyond picking funds.

Retirement’s Rising Costs: The Quiet Squeeze

Retirement today looks very different than it did for previous generations. Pensions that once provided steady monthly income are now rare, leaving most retirees to rely on a combination of Social Security, personal savings, and investment income. On the surface, that may seem perfectly sustainable—but the costs retirees face today are growing faster than the income sources meant to support them.

Staying Active After 60: A Key Investment in Your Retirement Years

When people think about preparing for a successful retirement, the focus often turns to investment portfolios, income strategies, and estate planning. While these financial steps are essential, there’s another investment that’s just as critical — and it can’t be measured in dollars: your physical health.

“It’s Gotta Be a CFP®”

Many people know October as Breast Cancer Awareness month, but it is also National Financial Planning Month, a built-in pause on the calendar to take stock of what’s working in your financial life and what isn’t. What areas are you excelling in and what opportunities might you be missing? According to the CFP® Board, it’s a natural time of year to focus on getting organized, especially ahead of year-end moves like tax planning, social security and benefits elections, and charitable giving.

When the Seasons Change, So Should Your Financial Plan

As summer fades and the crisp air of fall begins to settle in, many of us naturally think about change. The leaves turn, routines shift, and the year’s end suddenly feels closer than ever. Just as fall is a season of preparation—harvesting, storing, and getting ready for the winter ahead—it’s also an ideal time to pause and review your financial life.

Longevity Isn’t Luck—It’s a Lifestyle

As a financial advisor, I spend a lot of time helping clients plan for a retirement that could last 20, 30— even 40—years. But here’s the question: What good is a long life if it’s not a healthy one? We’re used to planning for “retirement income longevity,” but a deeper, richer conversation emerges when we shift the lens to something even more valuable: healthspan—the quality of life during those extra years.

Your 401(k) Could Be Changing—Here’s What Trump’s Order Means

Would you ever imagine holding cryptocurrency, private equity, or real estate inside your 401(k)? For decades, those kinds of investments were off-limits to the average retirement saver. But now, that possibility may be closer than you think.

Building a Retirement Portfolio: What Every Investor Should Know

In the years leading up to retirement, your investment strategy may have been focused on accumulation, maximizing growth, taking calculated risks, and riding out market volatility. But as you enter or approach retirement, the strategy must evolve. Now, it’s not just about growing your assets; it’s about preserving what you’ve built, generating income, and ensuring your portfolio supports a lifestyle that could last 25 to 30 years or more.

Whether you’re five years away from retirement or already there, building a durable and strategic retirement portfolio is essential. Here’s what every investor should know.

The 5 Biggest Retirement Mistakes You Can Still Avoid

Retirement is often thought of as the finish line—but in reality, it’s the beginning of a whole new chapter. After years of saving and investing, the decisions you make in retirement can have just as much impact on your financial security as the choices you made to get there.

And unfortunately, some of the most costly retirement mistakes happen after the paychecks stop.

Whether you’re a few years away from retirement or already living it, here are five common pitfalls to watch out for—and more importantly, how you can avoid them.

Diversifying Your Portfolio After Retirement

In the years leading up to retirement, you may have relied on the simplicity of target-date funds or asset allocation strategies designed to reduce risk as your retirement date approached. Now what? You’ve crossed that milestone—but retirement isn’t the finish line. You still have many years ahead, and you need your portfolio to perform well while continuing to manage risk. That’s where intentional diversification becomes critical.

The Debt Storm Ahead: How Rising U.S. Interest Payments Could Impact You

In the realm of personal finance and investment strategy, few forces are as powerful—and as underestimated—as the ripple effects of U.S. government debt. As of mid-2025, the national debt has surpassed $36 trillion, and while headlines often fixate on that staggering figure, the real threat lies not in the size of the debt, but in the growing cost to sustain it. If you're a retiree or an investor planning for the long term, the implications are enormous.

Why True Readiness for Retirement Goes Beyond Quitting Work

Retirement is often painted as the golden destination after decades of hard work—a well-earned reward marked by freedom, leisure, and the chance to finally relax. But while it may seem like the finish line of a long career, retirement isn't just about leaving the office behind. In fact, true readiness for retirement goes far beyond simply quitting work.